Hyundai Rotem Valuation Lowest Among Korea Defense Five as Q2 Meets Views

Hyundai Rotem is drawing attention for having the lowest relative valuation among Korea’s five leading defense companies. Second-quarter results are expected to match market expectations. The existing target-price reference is 283,000 won, with orders, delivery timing and margins driving the investment case.

Hyundai Rotem is again in focus as the lowest-valued company among Korea’s five major defense names. The key market view on June 29 is straightforward: although defense-export expectations have lifted the sector, Hyundai Rotem’s valuation remains relatively lower than peers when measured against earnings estimates. Its second-quarter performance is also expected to broadly meet consensus, limiting the risk of a near-term earnings shock.

Valuation Stands Out

The company’s appeal rests on the combination of defense growth and a relatively modest valuation multiple. Compared with other Korean defense majors, Hyundai Rotem still trades in the lower range even as expectations for earnings improvement remain intact. That leaves room for further re-rating within a sector that has already gained attention. The existing target-price reference is 283,000 won. For Korean investors, order backlog, delivery schedules and margin improvement will decide whether the won-denominated valuation can be sustained.

Q2 Earnings in Line

Second-quarter earnings are expected to come in close to market expectations. Defense sales tied to major programs such as the K2 tank should support revenue recognition, while the rail business remains a swing factor for profitability. Investors will focus less on sales growth alone and more on whether operating margins stay stable. Large defense contracts can be recognized at different points depending on delivery and progress, so full-year earnings visibility matters more than a single quarter.

Market Impact and Outlook

Hyundai Rotem’s low-valuation case matters for sentiment across Korean defense stocks. Korean defense companies have strengthened their global profile through export contracts, including European demand, and a weaker won can improve translated export revenue. Still, defense stocks remain sensitive to government approvals, delivery inspections, contract timing and foreign-exchange moves. The next checkpoints are second-quarter results, new order announcements and the speed at which existing contracts turn into revenue.

Key points

- Hyundai Rotem is drawing attention for having the lowest relative valuation among Korea’s five leading defense companies. Second-quarter results are expected to match market expectations. The existing target-price reference is 283,000 won, with orders, delivery timing and margins driving the investment case.

- Use the body and FAQ context before acting on this update.

- Compare with related issues inside the category hub.

FAQ

Why is Hyundai Rotem in focus?

It has the lowest valuation among Korea’s five major defense stocks and its second-quarter earnings are expected to meet consensus.

What is the target-price reference for Hyundai Rotem?

The existing target-price reference is 283,000 won.

What are the key earnings variables?

Backlog conversion, K2 tank delivery schedules, rail profitability and exchange-rate movements are the main variables.

Latest stories

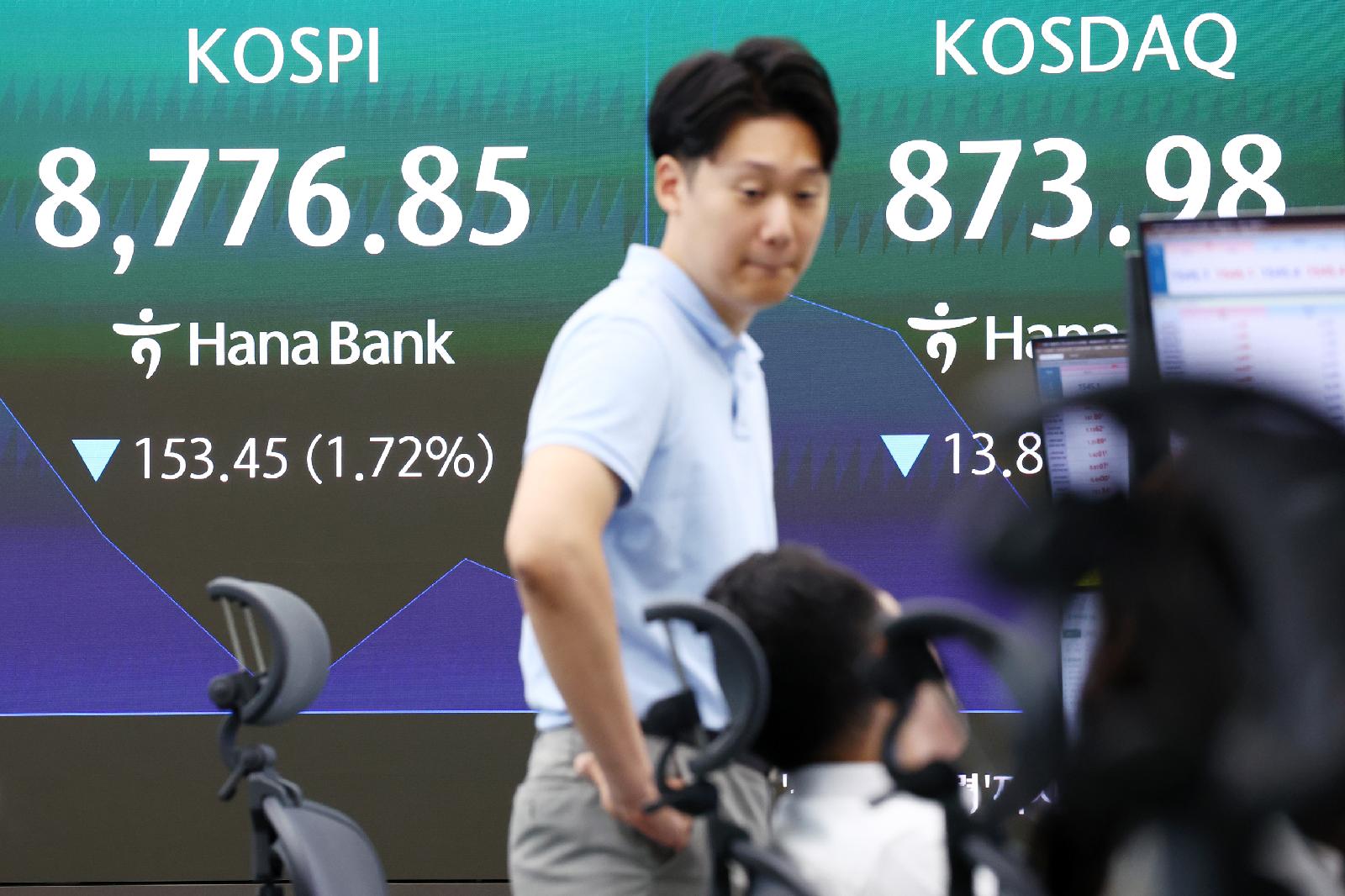

KOSPI Sinks as AI Investment Fears and Apple Price Hike Rattle Memory Demand

The KOSPI dropped nearly 6% on the 26th under heavy selling by foreign and institutional investors. Apple’s expected product price increases raised concerns that consumer replacement demand could slow, pressuring memory semiconductor orders. Korean chip and technology shares now face renewed valuation pressure tied to AI investment expectations.

KOSPI 150x and Samsung-SK Hynix 50x Leverage Ignite Korean Stock Futures Debate

Highly leveraged Korean equity futures have put investor protection back in focus. KOSPI-linked products can reach 150x leverage, while Samsung Electronics and SK Hynix products can reach 50x. Domestic investors appear to be using overseas access routes as semiconductor optimism fuels speculative demand.

KOSDAQ chip materials and equipment shares extend solo rally as institutions buy

KOSDAQ semiconductor materials, parts and equipment stocks outperformed during a broad market pullback. Profit-taking weighed on large chipmakers, but institutional money moved into supply-chain companies. Investors are watching second-round beneficiaries of a semiconductor recovery and Korea’s localization trend.

KOSPI Rally Raises False-Rally Warning as ETFs, Blue Chips and Dividends Flash Risks

The KOSPI’s advance does not fully reflect the health of the broader market. Three warning signs stand out: more falling stocks than rising ones, ETFs drifting away from fair value, and blue-chip shares turning into speculative trades. Even 5% dividend yields are being overlooked as short-term momentum dominates.

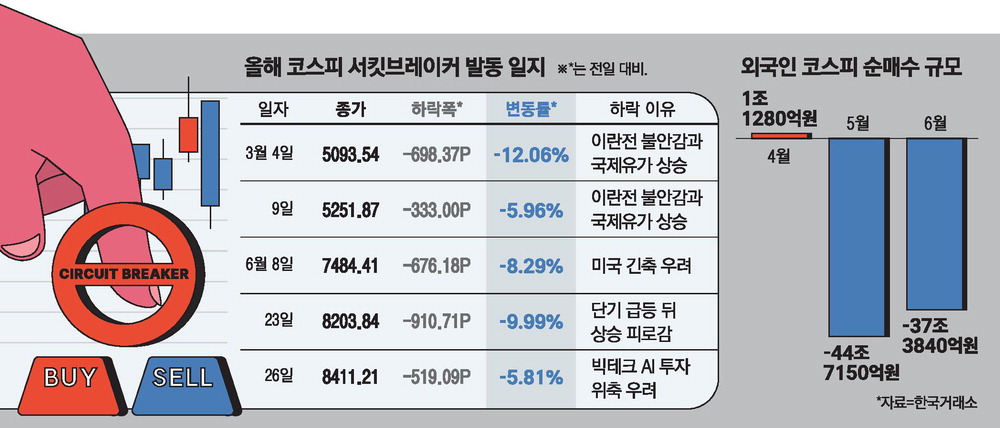

Korean Stock Market Volatility Surges as Sidecars and Circuit Breakers Hit Trading

Korean equities are moving through an unusually volatile phase, with daily moves of 4% to 5% or more. Buy-side and sell-side sidecars, as well as circuit breakers, have been activated. Profit-taking, heavy concentration in semiconductor shares and leveraged trading are widening index swings. Investors now need to watch won-based returns, FX moves and credit

Samsung Electronics and SK Hynix Slump Tests Global AI Chip Sentiment

Samsung Electronics and SK Hynix have become central gauges for global AI chip sentiment. Their decline triggered broader weakness in U.S. and European technology stocks. Investors are reassessing profit-taking, AI server demand and the pace of memory recovery. Micron’s earnings now stand as the next key checkpoint.

Perpetual Futures Expand From Bitcoin to Stocks, Commodities and Private Shares

Perpetual futures are leveraged derivatives that track asset prices without an expiry date. The market is expanding from Bitcoin and Ether into equity indexes, commodities and private-company exposure. U.S. volumes have already reached multibillion-dollar scale, while Korea must reconcile spot-centered crypto markets with derivatives oversight and investor p

Samsung C&T Target Rises Toward 700,000 Won on Samsung Electronics Stake and Nuclear Momentum

Samsung C&T is being re-rated sharply in the Korean market. Gains in Samsung Electronics and other affiliates have lifted the value of its holdings, while dividend expectations strengthened investor demand. Nuclear infrastructure momentum has added a growth angle, putting a 700,000 won target and strong buy case in focus.