KOSPI Rally Raises False-Rally Warning as ETFs, Blue Chips and Dividends Flash Risks

The KOSPI’s advance does not fully reflect the health of the broader market. Three warning signs stand out: more falling stocks than rising ones, ETFs drifting away from fair value, and blue-chip shares turning into speculative trades. Even 5% dividend yields are being overlooked as short-term momentum dominates.

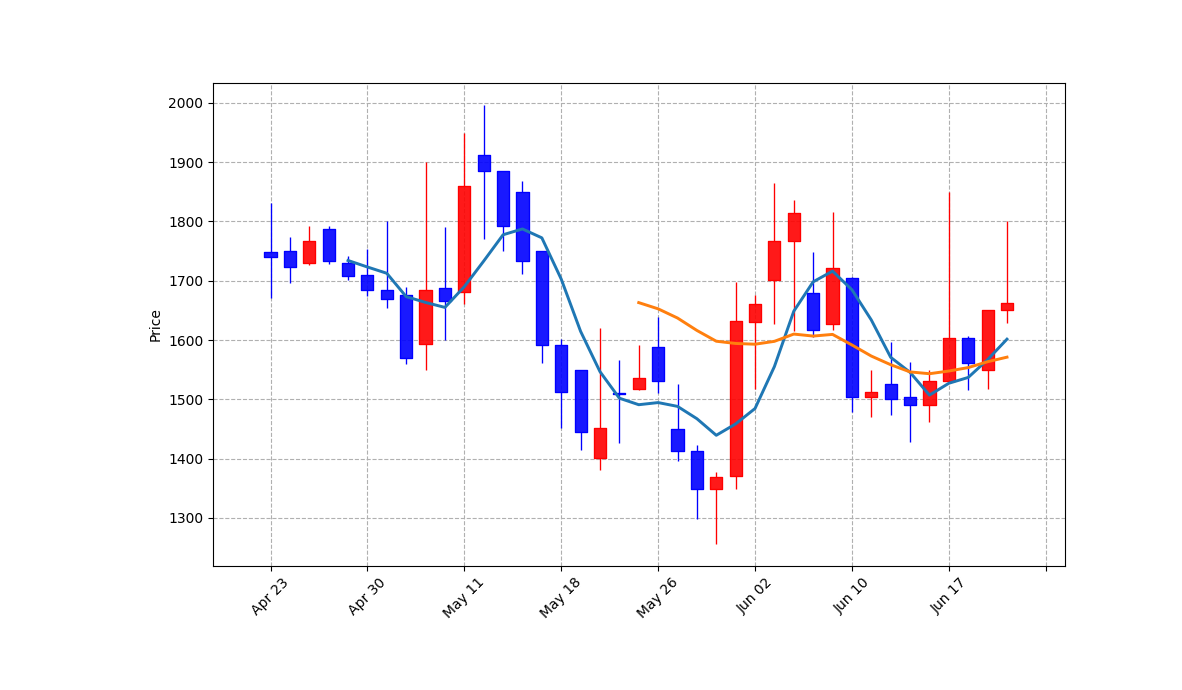

The KOSPI is rising, but the anxiety behind the rally is rational. The index advance does not automatically mean Korean equities are improving across the board. Current trading is concentrated in a limited group of large stocks and theme-driven products, creating a gap between index performance and what many investors actually experience.

Narrow Market Breadth

The first warning sign is internal weakness. On days when the KOSPI climbs, the number of declining stocks can still exceed advancing stocks. That is a classic false-rally pattern: a few heavyweight names lift the index while many shares remain weak. For Korean investors, this matters because the market is heavily influenced by sectors such as semiconductors, batteries, finance and holding companies.

ETFs and Blue Chips Turn Speculative

The second signal is distorted ETF pricing. ETFs are designed for low-cost, diversified exposure, but when money floods into a theme, trading heat can run ahead of underlying value. Investors may buy the product name and recent return rather than the assets inside. The third signal is the speculative treatment of blue chips. Companies that should be valued on cash flow, balance sheets and shareholder returns are increasingly traded for short-term price swings.

Dividends and Reform Become the Test

A market that ignores stocks offering dividend yields near 5% is showing a preference for momentum over value. Korea’s next test is whether corporate governance and shareholder returns improve as commercial law reform remains in focus. If companies respond only cosmetically, hopes of narrowing the Korea discount will weaken. A durable KOSPI rally needs broader participation, reasonable ETF pricing and renewed respect for dividends.

Key points

- The KOSPI’s advance does not fully reflect the health of the broader market. Three warning signs stand out: more falling stocks than rising ones, ETFs drifting away from fair value, and blue-chip shares turning into speculative trades. Even 5% dividend yields are being overlooked as short-term momentum dominates.

- Use the body and FAQ context before acting on this update.

- Compare with related issues inside the category hub.

FAQ

Why can the KOSPI rise while investors remain uneasy?

Because the index can be lifted by a small number of large stocks while more individual shares decline, weakening the broader market signal.

What is the ETF risk in this rally?

If thematic demand pushes ETF prices ahead of underlying value, ETFs can behave more like speculative products than diversified tools.

Why does a 5% dividend yield matter?

It is a concrete measure of cash return. Ignoring it in favor of price jumps suggests a short-term trading mindset.

Latest stories

Korea Stock Settlement Roadmap Set for October, Sale Proceeds Due Next Day

Korea is preparing a roadmap to shorten the stock trading settlement cycle in October. Once implemented, investors will be able to receive sale proceeds the day after selling shares. The reform will affect retail cash flow, brokerage operations, clearing, custody and foreign investor processes. It is also expected to strengthen confidence in the domestic cap

Nikkei 225 Closes Above 72,000 for First Time as Japan Rally Extends

The Nikkei 225 closed above 72,000 for the first time after eight consecutive gains. Semiconductor equipment makers, exporters and large manufacturers led the move. For Korean investors, yen exposure, Korea-listed Japan ETFs and allocation between Kospi and Japanese equities now matter more.

Single-Stock 2x ETFs Face Scrutiny as Korea Regulator Warns on Broker Gains

Korea’s single-stock 2x ETFs tied to Samsung Electronics and SK hynix have drawn a sharp regulatory warning. FSS Governor Lee Chan-jin sees a structure that benefits brokerages more reliably than retail investors. Daily 2x leverage can magnify both gains and losses. Sales practices and risk disclosures in Korea’s ETF market are likely to face closer review.

KOSDAQ Value-Up Guideline Set for July, Tied to Tier Review and Special Listings

The KOSDAQ value-up program enters a new phase in July. The guideline reflects growth-stage companies, technology-special listing structures and mid-cap market realities. With disclosures covering only 31% by market capitalization, tier reviews and special listing maintenance are expected to become key incentives.

SK Hynix Overtakes Samsung Electronics to Become KOSPI's Top Market-Cap Stock

SK Hynix became the largest KOSPI stock by market capitalization at 12:50 p.m. KST on June 22, 2026. It was the first time the company moved above Samsung Electronics in the ranking. AI semiconductors and high-bandwidth memory demand drove a sharp reassessment of won-denominated value. Investors are watching index weights, passive flows and the durability of

Kospi Above 9,000 Faces Key Test From Micron Earnings and U.S. PCE Inflation

The Kospi’s first move above 9,000 marks a major psychological shift for Korean equities. This week’s focus is Micron’s earnings and the U.S. PCE price index. Semiconductor demand, rate expectations and won-denominated returns will decide whether the rally can hold.

Golden Cross Stocks Jusung Corporation and Bistos Draw Attention in Korea

Jusung Corporation and Bistos have been identified as golden cross breakout stocks in the Korean market. A golden cross signals that short-term moving averages have moved above longer trend lines. The signal can improve sentiment, but trading volume, filings and company-specific momentum still matter.

MSCI Developed-Market Gate Looms as Kospi 9000 Sets Up Korea’s 10000 Test

The Kospi has crossed 9000, but the bigger market question is whether Korea can move beyond emerging-market treatment in MSCI’s framework. The index needs roughly 11.1% more to reach 10000. Currency access, settlement rules, dividend processes and English disclosure are central to the next rerating.