KOSPI at 8,000 Still Looks Cheap as Korea’s Low-PBR Stocks Face a Test

The KOSPI has entered a powerful long-term rally, but the broader Korean market is not uniformly expensive. Semiconductor giants have lifted the index, while many listed companies still trade below book value. Firms without a credible growth path face pressure to return capital through dividends and buybacks. Korea’s next re-rating will depend on shareholder

A KOSPI 8,000 era does not end the debate over Korea’s stock market discount. The index has reached new highs and has outperformed the S&P 500 over key long-term periods, but the rally is heavily shaped by large semiconductor names. Excluding that effect, more than half of Korean listed companies still trade below 1 times price-to-book value. That means the market values many firms at less than their accounting net assets.

Semiconductors Mask the Broader Market

The KOSPI began near 100 in January 1980 and has climbed through currency crises, global financial shocks and the pandemic. The move toward 8,000 reflects stronger Korean exporters and larger corporate earnings. Yet the index cannot be read as a full-market re-rating. Semiconductor leaders tied to artificial intelligence investment have done much of the lifting, while many domestic, industrial and mid-cap names remain overlooked.

A PBR below 1 sends a clear message. Investors doubt whether assets and cash on the balance sheet can produce enough future profit. Weak return on equity, vague capital allocation, limited dividends and unclear growth plans all keep valuations depressed. The Korea discount is no longer only about macro risk; it is about whether boards can earn more than their cost of capital.

Without Growth, Cash Should Go Back

Companies with real growth prospects must prove them through investment, exports, research and future cash flow. Companies without that proof need to raise dividends, buy back and cancel shares, or reduce debt. Korea’s value-up agenda points in the same direction. The market wants numbers, not slogans: target returns, payout ratios and capital plans.

For investors, the next phase is likely to be selective. A continuing semiconductor cycle may support the headline KOSPI, but low valuation alone is not enough. Stocks need a clear reason for the discount to narrow. Firms that improve return on equity and shareholder returns can break away from low PBR levels. Firms that simply hold cash without a convincing plan risk falling further behind.

Key points

- The KOSPI has entered a powerful long-term rally, but the broader Korean market is not uniformly expensive. Semiconductor giants have lifted the index, while many listed companies still trade below book value. Firms without a credible growth path face pressure to return capital through dividends and buybacks. Korea’s next re-rating will depend on shareholder

- Use the body and FAQ context before acting on this update.

- Compare with related issues inside the category hub.

FAQ

Why can Korean stocks still look cheap after a strong KOSPI rally?

Because much of the index gain is concentrated in semiconductor leaders, while more than half of listed companies remain below 1 times book value.

What does a PBR below 1 mean?

It means the market values a company below its book net assets, often because investors doubt its profitability, growth or capital allocation.

What should low-growth companies do?

They should improve capital efficiency through dividends, share buybacks, cancellations and clearer balance-sheet discipline.

Latest stories

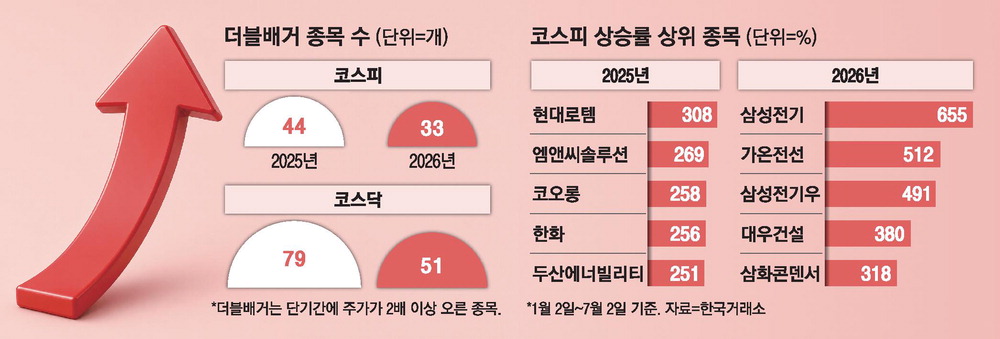

AI concentration cuts double-bagger stocks by 32% as Korea’s rally narrows

Korea’s 2026 stock rally has become narrower. The number of double-bagger stocks, or shares that rose more than 100%, is down 32% from the same period last year. Buying has centered on AI semiconductors, power infrastructure and data-center supply chains, leaving many non-AI sectors behind. Investors now need to weigh earnings visibility, valuation and won-b

KOSDAQ delisting drive accelerates as about 50 exits loom this year

KOSDAQ is moving into a sharper cleanup phase in its 30th year. Companies failing to meet market-capitalization requirements are the main focus. Around 50 firms may be delisted before year-end. Investors in illiquid and low-cap names need to check trading suspension and forced exit risks.

Semiconductor Stocks Slide as Meta AI Spending Debate Hits Market

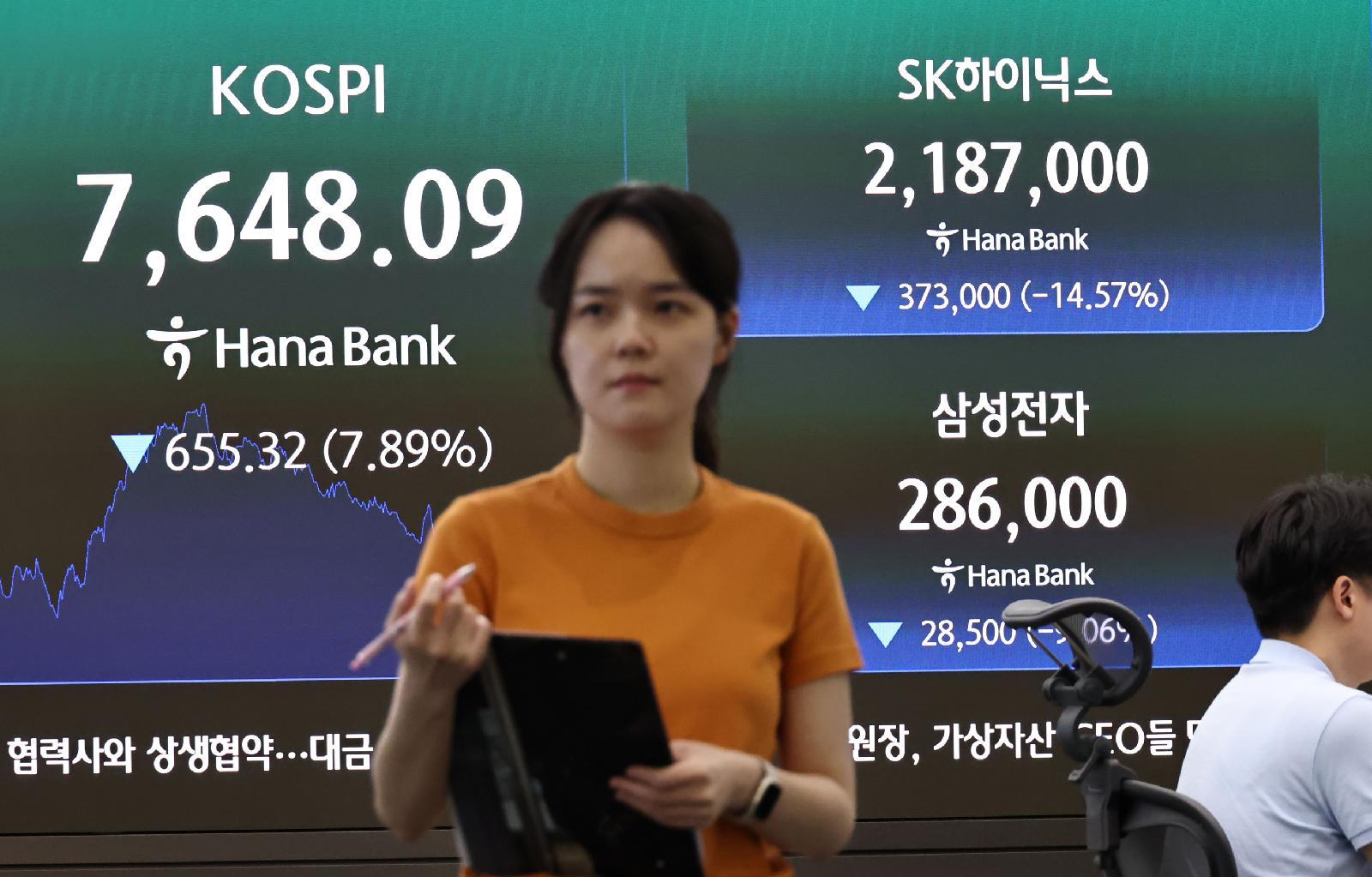

Semiconductor stocks fell sharply as Meta’s data-center and cloud ambitions revived concern that AI infrastructure spending may be running ahead of returns. The Kospi dropped 7% to close at 7,648, while SK Hynix moved toward its steepest decline in 17 years. Investors are now reassessing AI demand, memory prices and big-tech capital expenditure.

Elite Investors Rotate From Samsung Electronics to Preferred Shares on Discount Bet

The morning flow on June 29 showed a clear rotation out of Samsung Electronics common shares and into Samsung Electronics preferred shares. SK Hynix, Samsung Electronics preferred shares and Square led net buying, while Samsung Electro-Mechanics, Samsung Electronics and DB HiTek led selling. The move keeps exposure to semiconductors but adds a valuation and

Korean Auto Stocks Lag as Semiconductor Rally Draws AI-Driven Capital

The center of Korea’s stock market rally has shifted decisively toward semiconductors. AI investment and HBM demand are pulling capital into chip leaders, while auto stocks remain sidelined. Earnings slowdown concerns, labor negotiations and cost pressures continue to limit a rebound.

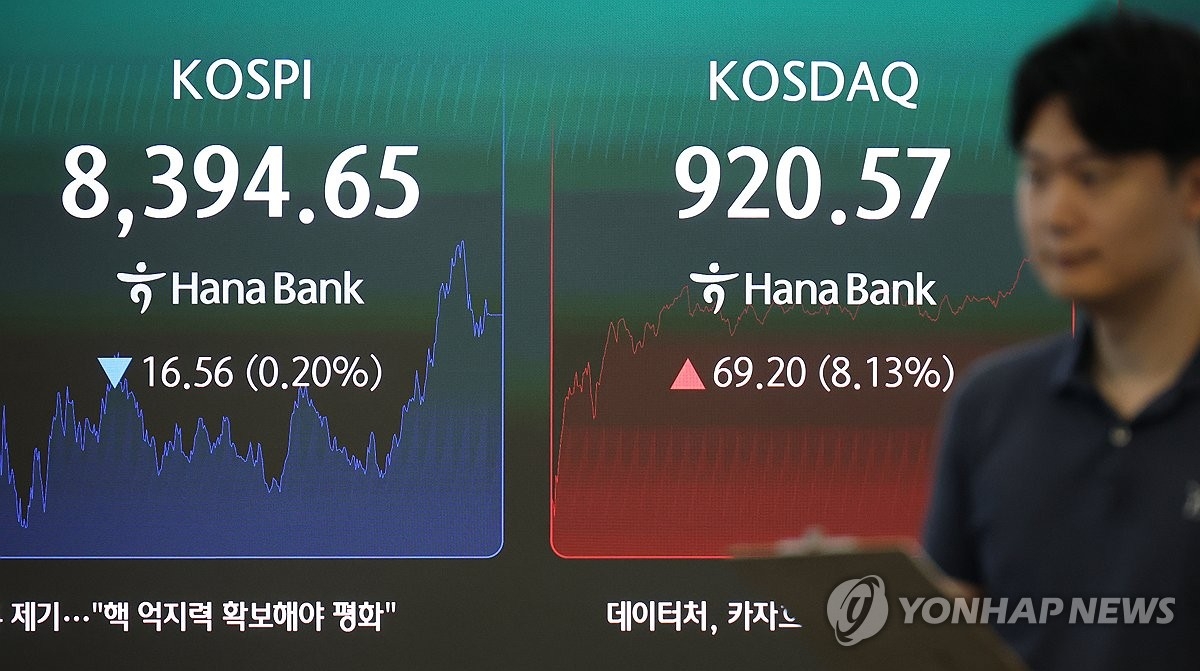

KOSPI Edges Lower as KOSDAQ Jumps 8%, Led by Batteries and Biotech

Korea’s stock market split sharply on the 29th. The KOSPI rose above 8,500 intraday but ended slightly lower near 8,300. The KOSDAQ, pressured for days, rebounded more than 8% to the 920 range as secondary battery, biotech and power shares attracted strong buying.

HYBE Sold After 9% Surge as Top Investors Buy Chips and Shipbuilding

Korea’s top-performing retail investors moved to sell HYBE after its sharp intraday rise on June 29. The flow pointed to profit-taking after a rapid 9% gain. Buying interest centered on Samsung Electronics, SK hynix, SK, and HD Hyundai Heavy Industries. The market preference leaned toward semiconductors and shipbuilding large caps.

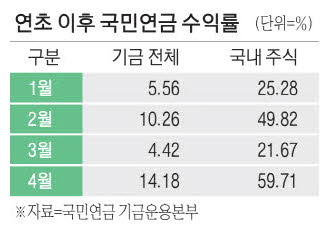

National Pension Domestic Stock Return Hits 60% as Fund Gains Reach 208 Trillion Won

Korea’s National Pension recorded a 14% total return as of the end of April 2026. Domestic equities delivered a 60% return, becoming the main driver of fund performance. Investment gains reached 208 trillion won. The Kospi’s move around 6,600 has become a key factor for pension finances and Korea’s capital market.