Semiconductor Peak-Out Debate Tests Samsung and SK Hynix Rally After AI-Led Surge

The rally in Samsung Electronics and SK Hynix has revived the semiconductor peak-out debate. The key is separating short-term profit-taking from the long-term AI memory cycle. HBM and data-center demand remain structural supports, while valuation, foreign flows and the won-dollar exchange rate remain risks.

The semiconductor peak-out debate has become the central question for Korean equities. Samsung Electronics and SK Hynix, often traded as the core memory pair, have risen sharply over the past year, forcing investors to ask whether the move is near exhaustion or still early in an AI memory supercycle. The clearest conclusion is that fear is coming first from short-term positioning, not from a settled collapse in industry demand.

Rally Meets Doubt

Korean chip stocks have been among the strongest performers globally, with major benchmarks and leading semiconductor names up around the mid-160% range over one year. After such gains, the same questions return: are earnings upgrades priced in, will memory price increases slow, and could AI server investment cool? The larger the winners, the faster profit-taking appears when liquidity becomes uneven.

Short-Term Flows Differ From Long-Term Demand

Commodity DRAM and NAND remain exposed to smartphones, PCs and inventory cycles. HBM, high-performance DRAM and server memory follow a different path. AI infrastructure spending, accelerator supply chains and cloud capex continue to support premium memory demand. For Samsung, HBM competitiveness and foundry losses are key. For SK Hynix, the question is how long its HBM lead can last.

What It Means For Korea Investors

The issue matters because chip megacaps drive the Kospi and foreign flows. A weaker won can lift exporters’ won-denominated earnings, but it also raises currency risk for overseas investors. Domestic institutions, short-selling rules and tax policy can add volatility. The right question is not whether semiconductors are over, but whether HBM shipments, memory prices, exchange rates and foreign buying confirm or reject the peak-out thesis.

Key points

- The rally in Samsung Electronics and SK Hynix has revived the semiconductor peak-out debate. The key is separating short-term profit-taking from the long-term AI memory cycle. HBM and data-center demand remain structural supports, while valuation, foreign flows and the won-dollar exchange rate remain risks.

- Use the body and FAQ context before acting on this update.

- Compare with related issues inside the category hub.

FAQ

What is the semiconductor peak-out thesis?

It is the view that chip earnings and pricing power may be near a cyclical high and could slow afterward.

Does it mean Samsung and SK Hynix must fall immediately?

No. Short-term profit-taking is possible, but long-term direction depends on HBM shipments and AI server demand.

What should investors watch?

HBM volume, memory prices, the won-dollar exchange rate, foreign net buying and semiconductor weight in the Kospi.

Latest stories

KOSPI at 8,000 Still Looks Cheap as Korea’s Low-PBR Stocks Face a Test

The KOSPI has entered a powerful long-term rally, but the broader Korean market is not uniformly expensive. Semiconductor giants have lifted the index, while many listed companies still trade below book value. Firms without a credible growth path face pressure to return capital through dividends and buybacks. Korea’s next re-rating will depend on shareholder

SK hynix draws elite investor buying as perceived value leads Korea chip trade

As of 2:30 p.m. on July 3, top 1% return investors were buying SK hynix most aggressively. DB HiTek also ranked among favored purchases, extending interest across chip stocks. Samsung Electronics led net selling but still rose, showing a split in semiconductor flows.

SK Hynix Jumps Over 10% as Institutional Buying Lifts KOSPI Back Above 8,000

SK Hynix led a powerful rebound in Korean equities on July 3 with a double-digit gain. Samsung Electronics and SK Hynix rose about 8% to 10%, putting semiconductors at the center of the KOSPI recovery. Institutional investors added roughly 4.4 trillion won net, helping the index close back above 8,000.

Meta neocloud review shakes chip stocks as SK Hynix buyers watch rebound

Meta’s review of a neocloud business has shaken Korean semiconductor sentiment. Investors who bought SK Hynix near 290,000 won are watching for a rebound, while Samsung Electronics holders are reassessing memory demand. The key question is whether idle compute sales slow new server investment or coexist with AI infrastructure expansion.

RWA Tokenization Gains Ground as 68% of Asian Investors Already Hold Assets

RWA tokenization is no longer a fringe digital-asset theme in Asia. Sixty-eight percent of high-net-worth and professional investors already hold tokenized real-world assets. About seven in ten are also willing to invest in tokenized stocks, raising pressure on market infrastructure and regulation.

Semiconductor Stocks Brake as Meta Cloud Plan Revives AI Peak-Out Fear

Meta's cloud business review triggered a reassessment of global semiconductor valuations. The key issue is whether available data-center compute points to slower AI server investment. GPU, HBM, foundry and advanced packaging names came under pressure, with Samsung Electronics and SK hynix central to Korea's market response.

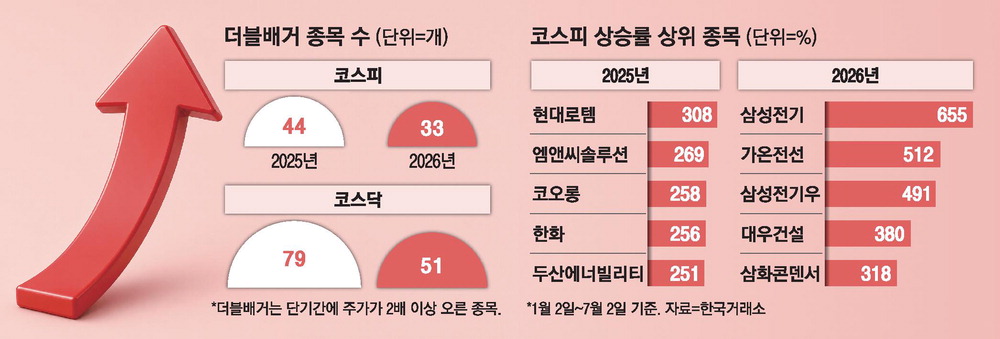

AI concentration cuts double-bagger stocks by 32% as Korea’s rally narrows

Korea’s 2026 stock rally has become narrower. The number of double-bagger stocks, or shares that rose more than 100%, is down 32% from the same period last year. Buying has centered on AI semiconductors, power infrastructure and data-center supply chains, leaving many non-AI sectors behind. Investors now need to weigh earnings visibility, valuation and won-b

KOSDAQ delisting drive accelerates as about 50 exits loom this year

KOSDAQ is moving into a sharper cleanup phase in its 30th year. Companies failing to meet market-capitalization requirements are the main focus. Around 50 firms may be delisted before year-end. Investors in illiquid and low-cap names need to check trading suspension and forced exit risks.